Interest rates are expected to inch up in more markets.

The European Central Bank raised rates 0.25% this week.

Bank of Japan raised rates an historic 1% earlier this week.

The Fed is seen as likely to raise rates at its June meeting.

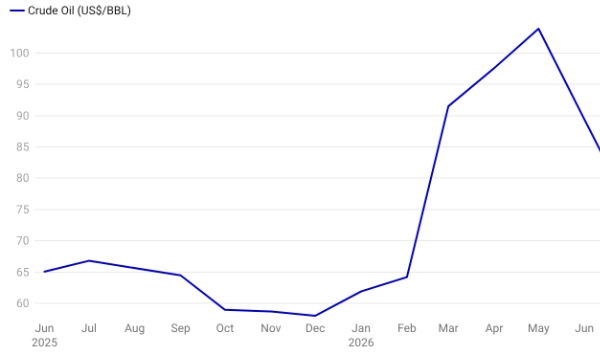

Oil prices continue to retreat, despite on going tensions in the Middle East.

Asian currencies (including the Phillipine peso, the Indonesian rupiah, the India rupee and the Thai baht) are trading at sharply lower levels as surging energy prices deplete US dollar reserves.

Logistics

Global freight rates rose sharply heading into peak, but still remain below year-ago levels.

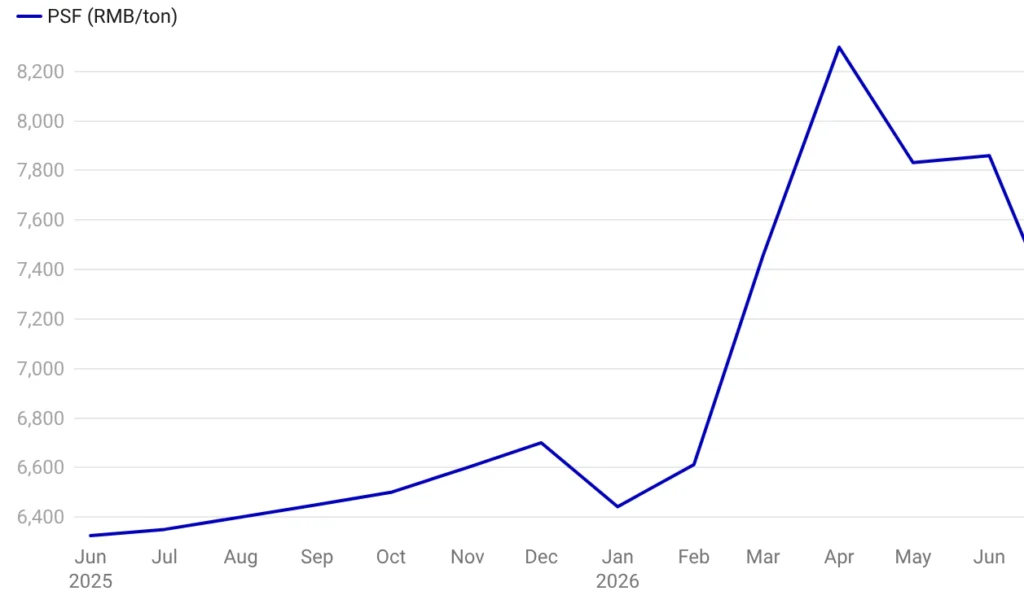

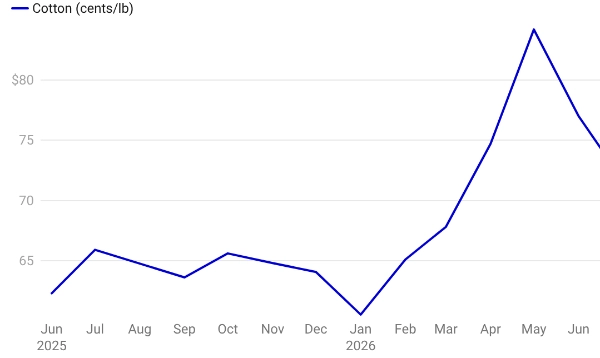

Materials prices are reteating, on lower oil prices. Wool however is still climibing.

Weekly Materials Prices | June 02, 2026

5 Signals We’re Watching in June

OIL PRICES. This is the lynchpin that’s driving up costs. As oil prices retreat, cost across the supply chain will start to fall.

LABOR COSTS. Wage pressure in key sourcing nations driving up costs for factories. Unlike energy and other costs, when wages go up they don’t come down.

TARIFF CHANGES. The US is actively pursuing Section 301 investigations – and key apparel producing nations are in the crosshairs.

CONSUMER DEMAND. Retail in key markets has remained resilient, but more purchases have been made using credit. That could slowdown future spending.

RETAIL PRICES. Brands can no longer lean as heavily on promotions to drive sales. Yet most might find it difficult to get consumers to pay more without offering tangibly better products.