Ocean rates up low double digits MoM; China–N. Europe air +35.5% MoM

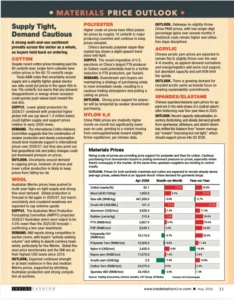

Supplier Pressure

Rising

↑

Lower MOQs, shorter lead times, reduced volumes, rising input and freight costs.

Top Shifts This Month

IFCI deteriorated again

50 → 47 month to month.

Cost shock is now sustained

Brent roughly $110–115/bbl by late April but down to ~$95/bbl by early May; oil up about 5–10% MoM and 60–80% YoY in the dashboard macro section.

Cotton jumped sharply

82.1 cents/lb, +17.0% MoM, +23.8% YoY.

Ocean and air freight moved higher

China–E. Coast +13.7% MoM; China–W. Coast +19.1% MoM; China–N. Europe air +35.5% MoM.

Order visibility is worsening

Lower MOQs, shorter lead times, reduced volumes; brands shifting to leaner, reactive sourcing.

Demand-side weakness is emerging

Retail demand holding but cautious, consumer confidence weakening across major markets.

Monthly Cycle Call

The apparel industry remains in Defensive territory, with rising costs, weakening confidence, and reduced order visibility pushing the market closer to Stress conditions heading into May.

Primary Risk: Sustained energy-driven cost pressure spreading into materials, freight, and factory operations.

Primary Opportunity: If energy prices stabilize, confidence could begin to recover and cost pressure may stop worsening.

Watch Next: Back-to-school ordering behavior, consumer sentiment, and whether buyers continue pushing micro orders and shorter cycles

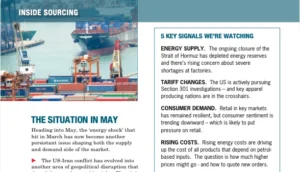

Current Industry Alerts

Fuel surcharges rising again — major carriers revised emergency fuel surcharges upward in April, with further increases/reset schedules for May.

Hormuz still not safe for transit — ships are still advised to avoid the Strait due to mine risk.

Gulf air cargo capacity still constrained — Dubai, Doha, and Abu Dhabi are at roughly 50–70% of pre-war capacity.

Section 301 investigations expanding pressure — key apparel-producing nations are in the crosshairs.

Brands pushing smaller orders — buyers are requesting micro orders and painfully tight lead times.

5 Signals We’re Watching

ENERGY SUPPLY. The ongoing closure of the Strait of Hormuz has depleted energy reserves and there’s rising concern about severe shortages at factories.

TARIFF CHANGES. The US is actively pursuing Section 301 investigations – and key apparel producing nations are in the crosshairs.

CONSUMER DEMAND. Retail in key markets has remained resilient, but consumer sentiment is trending downward – which is likely to put pressure on retail.

RISING COSTS. Rising energy costs are driving up the cost of all products that depend on petrol-based inputs. The question is how much higher prices might go – and how to quote new orders.

PRICING POWER. In a tight market will brands be able to raise retail prices enough to offset the higher cost of producing products?

Materials Prices | Week of May 12, 2025

Materials Prices (Trend)

Ocean Freight Rates

Air Cargo Rates

Ocean Freight Rates Trend

Air Cargo Rates Trend

Regional Barometer

Most Stable Region: USA.

Strongest Retail Momentum: Southeast Asia.

Greatest Volatility Risk: EU / UK.

Supply Chain Watchpoint: Southeast Asia.

Key Market Indicators

Brent Oil: roughly $95/bbl retreating in early May; +5–10% MoM; +60–80% YoY.

Inflation Trend: re-accelerating, especially in US and UK.

Policy Bias: tightening bias from Fed, BoE, and ECB.